Executive Summary

- April 2026 was the month the AI race became less about isolated benchmark wins and more about distribution, compute, and control: the biggest moves were deal resets, cloud partnerships, chip commitments, and policy actions rather than a single knockout model launch. (1)

- Anthropic had the strongest momentum month. It launched the cybersecurity-focused Mythos preview under Project Glasswing, rolled out Opus 4.7 and Claude Design, expanded AWS capacity to as much as 5 gigawatts, and deepened its Google/Broadcom compute relationship while reported new financing discussions underscored its rise from model vendor to infrastructure-scale platform company. (2)

- OpenAI’s alliance reset with Microsoft was arguably the month’s most consequential commercial event. The revised agreement ended Azure’s exclusive resale position, preserved Microsoft as primary cloud partner, and opened the door for OpenAI to distribute products across AWS and other clouds. Within a day, OpenAI brought GPT-5.5, Codex, and Bedrock Managed Agents to AWS. (3)

- Google used Cloud Next 2026 to make its clearest monetization case yet: Gemini Enterprise Agent Platform, eighth-generation TPUs split between training and inference, and evidence that AI spending is being routed into cloud revenue, security, and real enterprise deployments such as Merck. (4)

- Meta made progress but not a clean comeback. Muse Spark showed that Meta’s superintelligence push is real, and the company locked in another $21 billion of CoreWeave capacity. But China’s order to unwind the Manus acquisition showed how vulnerable cross-border AI strategy has become to national-security controls. (5)

- Governments moved from abstract AI debates to operational intervention. The EU struggled to simplify the AI Act while broadening DMA attention to AI and cloud. Japan set up a financial task force in response to Mythos-related cyber concerns. China tightened rules around digital humans and AI content labeling. (6)

- China’s AI story shifted from “cheap models” to “sovereign stacks.” DeepSeek-V4 did not shock markets the way prior DeepSeek releases had, but it intensified demand for Huawei’s Ascend chips among major Chinese internet groups, reinforcing the strategic importance of domestic hardware under export controls. (7)

- Monetization pressure kept rising. Reuters estimated the four U.S. hyperscalers were on track to spend around $600 billion on AI in 2026, even as investors kept asking whether cloud growth, ad gains, and enterprise software demand are sufficient to justify the buildout. (8)

Full Article

As of April 29, 2026, the clearest conclusion from the month is that frontier AI competition has entered a new phase. The center of gravity moved away from a simple “which lab has the best model?” narrative and toward a harder set of questions: who controls distribution, who can secure enough compute, who can prove enterprise value, and which governments will tolerate or constrain deployment. OpenAI and Microsoft reset the most important partnership in the sector; Anthropic turned frontier cybersecurity into a market and policy issue; Amazon and Google committed new infrastructure and capital; and Meta tried to reassert itself while colliding with geopolitics. (1)

The single most important commercial development was the OpenAI-Microsoft reset. OpenAI’s April 27 announcement said Microsoft remains its primary cloud partner, that OpenAI products will still ship first on Azure unless Microsoft declines to support required capabilities, and that Microsoft’s license to OpenAI IP through 2032 is now non-exclusive. Reuters added that Microsoft retains a guaranteed 20% cut of OpenAI revenue through 2030, subject to a cap, and that the renegotiation removed the old AGI rider while easing antitrust pressure and freeing OpenAI to sell through clouds such as AWS and Google Cloud. This changed the structure of the market, not just a product catalog: OpenAI is now materially less captive, and Microsoft is materially less exclusive. (3)

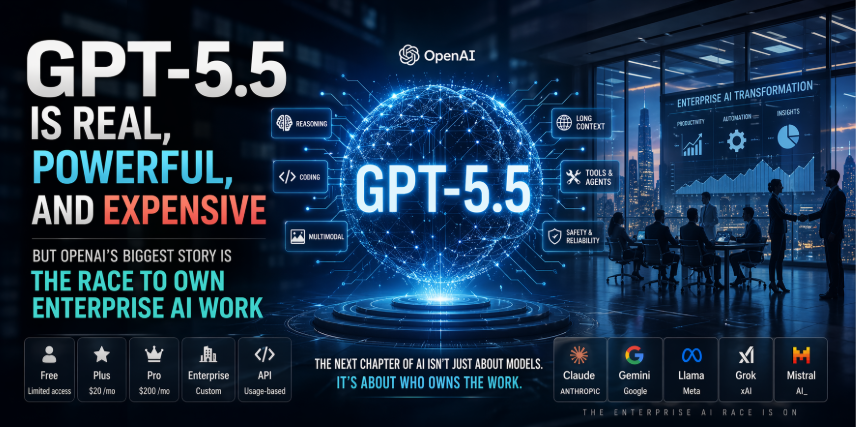

OpenAI then moved immediately to exploit that new freedom. On April 28, it announced that GPT-5.5, Codex, and Bedrock Managed Agents would come to AWS in limited preview. OpenAI’s own post said GPT-5.5 would be available on Amazon Bedrock and that Codex had surpassed 4 million weekly users; AWS said Bedrock Managed Agents would let customers deploy production-ready OpenAI-powered agents with AWS governance, identity, and data controls. Reuters added a striking commercial detail: Amazon and OpenAI have reportedly deepened ties to the point that Amazon invested $50 billion in OpenAI, while OpenAI committed to spend $100 billion on AWS over eight years and use two gigawatts of Trainium-backed compute. Even if those capital terms sit partly outside the official product announcement, the directional message is unmistakable: frontier AI is becoming a multi-cloud utility business, not a single-vendor stack. (9)

GPT-5.5 itself mattered because it reinforced the industry’s move toward agents that can carry more of the workflow rather than merely answer prompts. OpenAI said GPT-5.5 improves agentic coding, computer use, knowledge work, and early scientific research, while matching GPT-5.4 latency and using fewer tokens on Codex tasks. It cited improved benchmark performance across Terminal-Bench 2.0, OSWorld-Verified, GDPval, BrowseComp, and CyberGym, and rolled the model out across ChatGPT Plus, Pro, Business, and Enterprise, with the API following on April 24. In other words, the product pitch shifted from intelligence as conversation to intelligence as execution. (10)

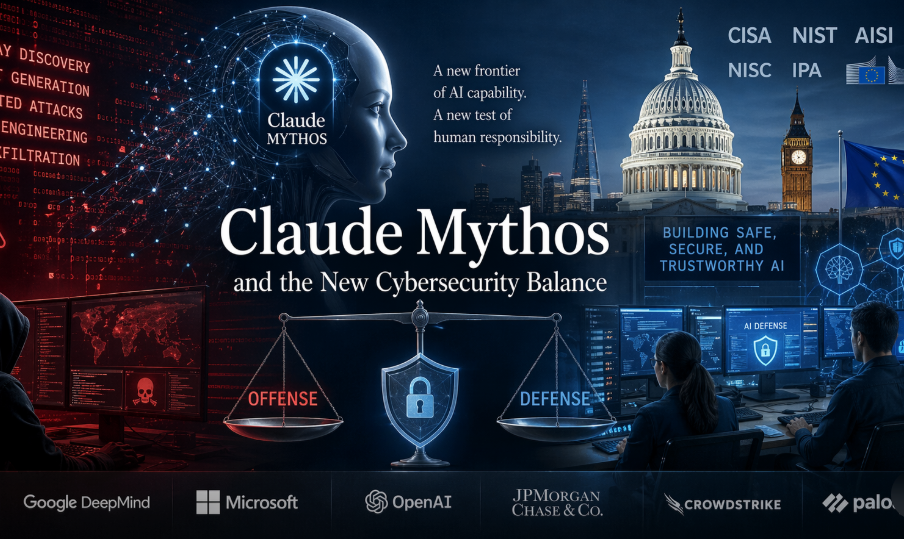

If OpenAI owned the month’s biggest alliance reset, Anthropic owned the month’s biggest momentum shift. Project Glasswing and Claude Mythos Preview took an emerging fear—AI-enabled cyber offense—and made it operational for companies, regulators, and governments. Anthropic said Glasswing launch partners included major infrastructure and security firms such as Amazon Web Services, Apple, Cisco, Google, JPMorganChase, Microsoft, NVIDIA, CrowdStrike, the Linux Foundation, and Palo Alto Networks. Reuters reported that Mythos was limited to around 40 heavyweight testers, that experts warned it could identify and exploit previously unknown vulnerabilities faster than companies can patch them, and that U.S. and U.K. officials, central bankers, and large banks moved quickly to assess the risk. Reuters also reported that U.S. software stocks sold off after the launch, a sign that investors no longer see “AI disruption” as theoretical. (2)

Anthropic then matched that policy shock with product and infrastructure breadth. It released Claude Opus 4.7 on April 16, positioned as a stronger model for coding, agents, and multi-step work, and launched Claude Design on April 17, pushing Claude further into visual documents, prototypes, and presentations. Reuters noted that Adobe responded with its own AI assistant and connector to Claude as competition heated up in creative software. The significance here was not any single benchmark; it was that Anthropic was expanding from “best coding model” territory into cybersecurity, enterprise workflows, and creative work at once. (11)

The bigger story, however, was compute. Anthropic’s April 20 announcement said it had signed a new agreement with Amazon securing up to 5 gigawatts of capacity, committing more than $100 billion over ten years to AWS technologies, and receiving a fresh $5 billion investment from Amazon with up to $20 billion more possible in the future. Anthropic also said it already used more than one million Trainium2 chips and had more than 100,000 customers running Claude on Amazon Bedrock. Earlier in the month, Anthropic said it had expanded its Google and Broadcom relationship for multiple gigawatts of next-generation TPU capacity, with most of the new infrastructure to be sited in the United States. Bloomberg, in a report summarized by Reuters, separately said Alphabet planned to invest up to $40 billion in Anthropic. Put together, these are not normal startup financing numbers; they are utility-scale industrial policy numbers. (12)

Google’s answer to all this came at Cloud Next. The company’s strategy looked less like “we will win because Gemini is best” and more like “we will win because we can operate the entire enterprise agent stack.” Google introduced Gemini Enterprise Agent Platform as a unified environment to build, govern, and optimize autonomous agents, while also supporting Anthropic models on the same platform. Sundar Pichai said Google’s first-party models now process more than 16 billion tokens per minute via direct customer API use, that paid monthly active users of Gemini Enterprise grew 40% quarter over quarter in Q1, and that just over half of the company’s machine-learning compute investment in 2026 would go to the cloud business. Google also unveiled TPU 8t for training and TPU 8i for inference, explicitly designing for an “agentic era” in which low-latency inference and cost discipline matter as much as training runs. Reuters reinforced the monetization angle by reporting that Merck plans to invest up to $1 billion over several years with Google Cloud to deploy AI across research, regulatory, manufacturing, and commercial operations. (4)

Meta’s April was more mixed. On the positive side, Reuters reported that Muse Spark was the first model from Meta’s costly superintelligence team and the first major Meta model release in about a year. Meta said it would power the Meta AI app and website first, then roll out across WhatsApp, Instagram, Facebook, Messenger, and its AI glasses. Reuters said the model was catching up in some categories but still lagged in coding and abstract reasoning, while Meta signaled clearer monetization plans around shopping, multimodal assistance, and product discovery. Infrastructure spending supported the seriousness of the push: Reuters reported Meta signed a fresh $21 billion CoreWeave agreement, extending through 2032 and giving it early access to NVIDIA’s Vera Rubin chips, while Meta said it could spend up to $135 billion on AI buildout this year. But the month also brought a geopolitical setback, when Reuters reported that China ordered Meta to unwind its $2 billion-plus Manus acquisition, warning that Chinese-linked AI talent and technology were effectively off-limits to U.S. buyers without Beijing’s approval. CoreWeave and NVIDIA both benefited from Meta’s need for outside compute, but Meta itself ended the month looking ambitious rather than clearly resurgent. (5)

Policy and national security also moved from backdrop to front line. The European Union failed to reach a deal on watering down parts of the AI Act, leaving businesses with continued uncertainty, while the European Commission said the Digital Markets Act would now turn more directly toward AI and cloud services and was examining whether certain AI services should count as core platform services. Japan launched a financial task force in response to Mythos-related cybersecurity fears, while Reuters reported that Google had reportedly signed a classified AI agreement with the U.S. Department of Defense, citing The Information. Because the Google-Pentagon story relies on secondary reporting and the agreement text is not public, it should be treated as reported rather than fully documented fact; but even as a report, it fits April’s broader pattern of frontier AI firms moving deeper into state and defense systems. (6)

Finally, April sharpened the geopolitical split around AI hardware. DeepSeek’s V4 did not repeat the market shock of earlier DeepSeek releases, but Reuters argued that the more important question was whether China could keep advancing with domestic chips. On April 29, Reuters reported that demand for Huawei’s Ascend 950 chips surged after DeepSeek optimized V4 for them, with ByteDance, Tencent, and Alibaba seeking new orders. That shift matters because it reframes the China story: not “can Chinese labs make interesting models?” but “can China sustain an AI ecosystem under U.S. restrictions using mostly Chinese hardware?” April’s evidence suggests the answer is increasingly “possibly yes,” even if supply constraints remain real. China also tightened draft rules around digital humans and AI labeling, reinforcing that Beijing wants both faster deployment and tighter state control. (7)

From a business perspective, the month ended with a familiar paradox. Reuters estimated that Alphabet, Amazon, Meta, and Microsoft are on track to spend around $600 billion on AI in 2026, and investors are still demanding proof that cloud acceleration, enterprise agents, and AI-enhanced advertising can justify that outlay. Yet April also supplied some of the clearest evidence so far that AI is moving from pilots to production: Merck is scaling dossier preparation globally with Google; Amazon is packaging agentic systems into hiring, supply-chain, customer-service, and health products; OpenAI and Anthropic are no longer talking about isolated APIs but about deployed platforms inside the world’s largest clouds. April 2026 did not settle the monetization debate. It did, however, make the shape of the battle much clearer. (8)

Top Stories

This ranking is analytical judgment based on market impact, capability significance, infrastructure consequences, policy relevance, and likely second-order effects.

- OpenAI and Microsoft reset the alliance.

This was the month’s most structurally important AI business story because it changed the rules of distribution. OpenAI gained permission to sell across clouds, Microsoft kept primary-cloud status and a non-exclusive IP license, and both sides reduced strategic ambiguity ahead of heavier monetization and possible IPO paths. (3) - Anthropic made frontier cybersecurity a boardroom and policy issue with Mythos and Project Glasswing.

The story mattered not only because of model capability, but because it triggered market selloffs, bank briefings, and government attention in the U.S., U.K., and Japan. That is real-world impact, not lab theater. (2) - Anthropic locked in industrial-scale compute from Amazon and Google.

Amazon’s up-to-5GW agreement and fresh investment, together with Anthropic’s Google/Broadcom TPU expansion and reported Alphabet financing plans, made Anthropic look like the strongest “AI utility customer” of the month. (12) - Google Cloud Next turned Google’s AI strategy into an enterprise platform story.

Gemini Enterprise Agent Platform, TPU 8t and 8i, explicit cloud monetization metrics, and scaling customer stories made April the clearest evidence yet that Google is trying to win the control plane for enterprise agents. (4) - OpenAI launched GPT-5.5 and quickly pushed it onto AWS.

GPT-5.5 advanced the “AI that executes work” narrative, and the AWS rollout turned that capability into a broader distribution event instead of an Azure-only upgrade. (10) - Meta launched Muse Spark and doubled down on external compute with CoreWeave.

The model showed Meta’s superintelligence program is producing frontier-class systems again, while the $21 billion CoreWeave deal underscored that Meta is willing to spend at hyperscale to stay relevant. (5) - China blocked Meta’s Manus acquisition.

This may prove to be a landmark precedent for cross-border AI M&A: Beijing signaled that Chinese-linked AI talent, data, and IP remain strategic assets even when companies relocate abroad. (13) - The EU pushed AI and cloud competition policy into a new phase.

The failure to finalize AI Act simplification and the Commission’s decision to examine whether AI and cloud services belong under stronger DMA scrutiny both matter because European rules increasingly shape global product design and go-to-market strategy. (6) - DeepSeek-V4 and the post-launch scramble for Huawei chips deepened the sovereign-AI story.

The muted stock reaction was itself informative: markets no longer panic at every efficient Chinese model. What mattered was the intensifying fit between domestic models and domestic accelerators. (7) - Military and national-security AI adoption expanded.

Reuters reported that Google had reportedly joined other firms in signing a Pentagon classified-work agreement, while governments simultaneously raced to adapt to cyber-capable frontier models such as Mythos. The exact Pentagon contract details remain partly opaque, but the directional shift is clear. (14)

Winners, Losers, and Trends

Winners: The clearest winner was Anthropic. Revenue scale, product breadth, cyber relevance, and compute access all improved at once, and the company emerged as the lab most successfully converting technical strength into enterprise and infrastructure leverage. Google Cloud also gained momentum, not because it “won” the model race outright, but because it strengthened its position as the agentic operating layer for enterprises while monetizing both its own models and partners’ models. AWS was another winner because it now hosts both Claude and OpenAI offerings more directly, which strengthens Bedrock’s role as a multi-model marketplace and enterprise deployment layer. Huawei was a conditional winner as DeepSeek-V4 drove renewed demand for domestic Chinese hardware. (12)

Losers: Microsoft did not have a bad month operationally, but it lost something strategically important: exclusivity. That reduction in control may eventually help Microsoft by freeing capacity and reducing regulatory pressure, but it also weakens the narrative that Azure is the singular home of OpenAI. Legacy software vendors also remained under pressure as investors reacted again to Anthropic-driven disruption fears. Meta’s month was mixed enough to place it in a “not yet recovered” category: Muse Spark was progress, but it did not establish clear model leadership, and the Manus setback exposed geopolitical risk in Meta’s AI strategy. Cross-border AI deals involving Chinese roots were obvious losers as a category. (1)

Trends: Three trends stood out. First, multi-cloud AI is replacing exclusive alliances. Second, compute commitments are now measured in gigawatts, not GPU anecdotes, which makes AI competition look increasingly like energy and industrial planning. Third, enterprise AI is moving from copilots to agents: the recurring language across OpenAI, Amazon, and Google was not “assist” but “deploy,” “orchestrate,” “govern,” and “execute.” A fourth trend is that security and sovereignty are no longer side issues. April showed that frontier AI now sits directly inside antitrust, cyber-defense, export-control, and military planning debates. (1)

Outlook for 2026

April’s developments suggest that the rest of 2026 will be shaped by distribution deals, infrastructure bottlenecks, and regulation at least as much as by model releases. The revised Microsoft-OpenAI arrangement makes it likely that more “exclusive” relationships across the stack will loosen or be re-written, especially where customers demand model choice and regulators dislike closed ecosystems. (3)

The second implication is that Anthropic and OpenAI will be judged less on demos and more on whether they can turn enormous compute access into durable enterprise revenue. Anthropic’s disclosed run-rate revenue growth and OpenAI’s AWS expansion both raise the bar for execution; at the same time, Reuters’ reporting on investor concern over AI spending shows that patience is not unlimited. That tension should define financing, IPO timing, and partner negotiations through year-end. (12)

Third, Google and AWS appear best positioned to benefit if enterprises continue preferring multi-model infrastructure rather than single-lab dependency. Google is building the control plane for agents; AWS is building the most commercially flexible model store and runtime. That does not guarantee either company wins, but it does suggest the next phase of competition is about operational gravity more than marketing buzz. This is an inference from the month’s announcements, not a settled fact. (15)

Fourth, policy pressure will probably intensify around two areas: competition and national security. Europe is already steering toward cloud and AI market-power questions; Japan’s reaction to Mythos shows how quickly frontier models can trigger sector-specific oversight; and reported Pentagon deals indicate that more governments will want privileged access to leading systems. Expect more fights over dual-use models, procurement guardrails, and model availability by jurisdiction. (6)

Finally, China’s trajectory looks increasingly bifurcated rather than backward. DeepSeek-V4’s muted reception did not signal weakness so much as normalization. If DeepSeek-class models continue to work well on Huawei silicon and Chinese platforms keep deploying them quickly, the rest of 2026 could bring a more durable split between U.S.-aligned and China-aligned AI stacks. (7)

Summary Table

| Date | Organization / Country | Headline | Category | Why It Matters |

|---|---|---|---|---|

| Apr. 27 | OpenAI / Microsoft | Partnership rewritten; Azure exclusivity ended | Partnership / enterprise | OpenAI can now distribute products across clouds while Microsoft keeps primary-cloud status and a capped revenue share, a structural change to AI commercialization.(3) |

| Apr. 28 | OpenAI / Amazon AWS | GPT-5.5, Codex, and Bedrock Managed Agents come to AWS | Product launch / enterprise adoption | This turned OpenAI from a primarily Azure-centered seller into a broader multi-cloud supplier and gave AWS a stronger position in enterprise AI deployment. (9) |

| Apr. 23 | OpenAI | GPT-5.5 released | Model release | OpenAI framed GPT-5.5 as a more agentic, efficient system for coding, knowledge work, and computer use, reinforcing the shift from chatbots to workflow execution. (10) |

| Apr. 7 | Anthropic | Project Glasswing and Mythos Preview launched | Research breakthrough / cybersecurity | Mythos pushed frontier AI into cyber-defense and cyber-risk debates, affecting software valuations and drawing attention from regulators and governments.(2) |

| Apr. 20 | Anthropic / Amazon | Up to 5GW of new compute and fresh Amazon investment | Infrastructure / funding | The agreement moved AI competition into utility-scale infrastructure, with Anthropic committing over $100 billion to AWS technologies over ten years. (12) |

| Apr. 6 and Apr. 24 | Anthropic / Google / Broadcom | TPU expansion; reported Google investment up to $40B | Infrastructure / financing | Anthropic deepened its TPU pipeline with Google and Broadcom, while separate reporting suggested Alphabet planned an even larger financial commitment. The combination underscored Anthropic’s strategic centrality. (16) |

| Apr. 22 | Cloud Next launches Gemini Enterprise Agent Platform and TPU 8t/8i | Enterprise platform / chips | Google made its strongest case yet that AI spending is turning into cloud products, security offerings, and enterprise agent infrastructure. (4) | |

| Apr. 8 and Apr. 9 | Meta / CoreWeave | Muse Spark debuts; Meta signs fresh $21B compute deal | Model release / infrastructure | Meta showed renewed model ambition and confirmed it is willing to buy massive external compute to stay in the frontier contest. (5) |

| Apr. 28 | China / Meta | Beijing orders Manus acquisition unwound | Geopolitics / M&A | The decision showed that Chinese-linked AI IP, talent, and data remain strategic assets and raised the regulatory risk premium on cross-border AI deals. (13) |

| Apr. 28 and Apr. 29 | European Union | AI Act simplification stalls; DMA focus broadens to AI and cloud | Policy / regulation | Europe signaled that AI governance will increasingly be about both safety rules and market structure, especially for cloud and assistant platforms. (6) |

| Apr. 27 and Apr. 29 | China / DeepSeek / Huawei | DeepSeek-V4 spurs scramble for Huawei Ascend chips | Semiconductors / geopolitics | The market did not panic, but domestic-model-plus-domestic-chip alignment became a more important strategic story than benchmark surprise. (7) |

| Apr. 22 and Apr. 24 | Google / Merck / Japan | Merck scales with Google Cloud; Japan launches Mythos task force | Enterprise adoption / government response | These two stories showed the same thing from opposite angles: AI is moving into production in regulated industries, and governments are reacting in operational rather than abstract terms. (17) |

Open Questions and Limitations

This report covers developments reported through April 29, 2026, so any major events on April 30 are necessarily excluded.

A few important stories remain partly uncertain. The reported scale of Alphabet’s planned Anthropic investment came from Bloomberg and Reuters rather than a detailed public filing; the reported Google-Pentagon AI deal came via Reuters citing The Information, and the contract text is not public; and Reuters’ large capital figures around the OpenAI-AWS relationship go beyond the narrower official product announcement. I have therefore treated those items as reported developments, not as fully disclosed contractual facts. (18)

Another limitation is that some high-profile April product announcements were limited previews rather than broad general availability. That is especially true for Mythos Preview, AWS/OpenAI Bedrock integrations, Bedrock Managed Agents, and some Meta and Anthropic releases. Their importance lies in what they imply about direction, capability, and market structure, not yet in universal deployment scale. (2)