Executive summary

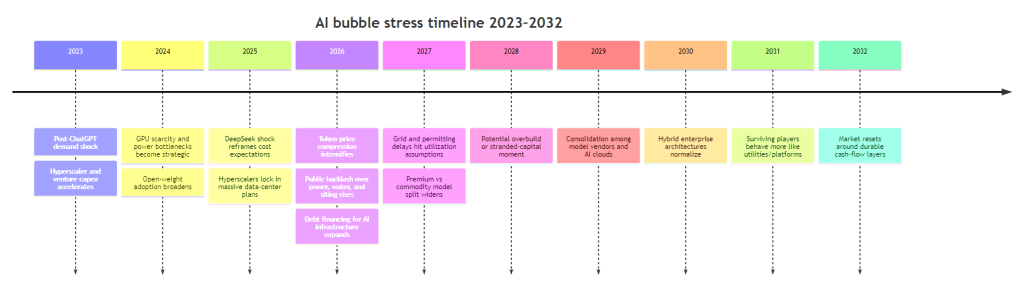

The most plausible “visible” AI bubble collapse is not a scenario in which artificial intelligence stops mattering. It is a scenario in which AI remains technically real and socially useful, but the financial claims built on top of it prove too large, too early, and too capital-intensive. The core mismatch is temporal: hyperscalers, utilities, and investors must commit long-duration capital to data centers, GPUs, networking, cooling, and power infrastructure, while model prices and software moats are compressing much faster than those assets can be built or depreciated. Goldman Sachs estimates roughly $7.6 trillion of AI-related capital spending between 2026 and 2031, while the IEA says the capital expenditure of five large technology companies exceeded $400 billion in 2025 and is set to rise another 75% in 2026.

The second pressure point is unit economics. Training remains expensive, but inference is the recurring cost center and the market price setter. A recent arXiv study finds about a 600-fold decline in token prices from 2020 to 2026, with a structural break around May 2024 as competition began driving price declines faster than pure hardware progress. Meanwhile, Reuters reported that DeepSeek made a 75% permanent cut to its flagship V4-Pro API pricing in May 2026, underscoring how quickly LLM capacity can be commoditized.

A visible collapse therefore becomes most likely when four conditions align: overbuilding of physical AI infrastructure, sharp compression in inference pricing, demand that is real but not profitable enough at forecast rates, and rising political resistance to the infrastructure build-out. That combination would not “end AI.” It would more likely force a three-tier market: premium frontier cloud models, low-cost commodity cloud models, and proliferating local/on-device models, with hybrid architectures becoming the default enterprise design.

What would make the bubble visibly crack

The visible crack would likely appear first in capital markets and project finance, not in model quality. Microsoft said it planned about $80 billion of AI-enabled data-center spending in fiscal 2025; Alphabet reaffirmed $75 billion of 2025 capex; Meta initially targeted up to $65 billion in 2025 and later raised annual capex guidance to $125–145 billion in 2026; Amazon has also turned to debt markets as AI capex accelerated. NVIDIA, by contrast, has remained the clearest near-term winner: in fiscal Q1 2027 it reported $81.6 billion of revenue, including $75.2 billion from Data Center, with gross margin near 75%.

That asymmetry is precisely what makes an eventual correction visible. Early in a build-out, upstream suppliers such as NVIDIA can monetize scarcity immediately, while downstream model providers and apps absorb price competition, cloud commitments, and support costs. Reuters reported that OpenAI burned $3.7 billion in the first quarter of 2026 on $5.7 billion of revenue, while a separate Reuters report said the company spent $34 billion in 2025 ahead of a planned IPO. That pattern is consistent with a market in which demand is strong, but monetization lags infrastructure and R&D intensity.

The timeline above is consistent with the current evidence base: hyperscaler capex surged after the generative AI shock; energy analysts increasingly expect power constraints in 2027–2028; and local or on-device inference is moving from niche to product reality.

Unit economics and demand elasticity

The crucial economic issue is that training is lumpy, but inference is perpetual. Training can create technical advantage; inference determines whether that advantage turns into durable gross margin. The “Tiered Super-Moore’s Law” paper finds not only dramatic token-price declines, but also that market concentration fell sharply as more vendors entered and competition intensified. A separate arXiv paper on reasoning models shows that listed API prices often understate true cost variation because “thinking tokens” can swing total request cost wildly across tasks. In other words, revenue forecasts based on posted prices can be misleading even before price wars intensify.

There is a genuine elasticity effect: lower prices unlock more use cases. Alphabet explicitly defended its capex by arguing that cheaper AI expands demand, and Reuters described customers such as Verizon and Intuit reporting visible business benefits from AI deployments. But elasticity does not guarantee adequate returns on fixed capital. Demand can rise while unit margins still collapse. This is the familiar danger of infrastructure-heavy growth industries: quantity grows faster than profits.

Technology trends reinforce that pressure. DeepSeek-R1 openly released distilled models derived from its larger reasoning system; Google’s Gemma family is explicitly positioned as lightweight open models for local deployment; Gemma 3 QAT models reduce memory requirements enough to run larger models on consumer GPUs; Microsoft’s Foundry Local lets developers run models on-device without Azure; and Apple’s Foundation Models framework exposes on-device and private-cloud options in a unified API. These trends erode the assumption that high-end cloud inference will capture all value.

Chip progress cuts both ways. NVIDIA’s Blackwell architecture adds FP4 and new quantization-friendly formats, promising major speed and efficiency improvements. That is bullish for adoption, but it is also bearish for the economic life of installed prior-generation silicon if customers can get much lower cost per token on newer stacks. Goldman explicitly warns that operational obsolescence can arrive faster than accounting depreciation schedules imply.

Infrastructure, politics, and the risk of stranded capital

The visible-collapse thesis becomes stronger because AI is not just software. It is electricity, water, land, cooling, transmission, and permitting. The IEA says data-center electricity use surged in 2025, and its April 2026 update says the capex of five large tech companies rose above $400 billion in 2025 and is set to climb again in 2026. Morgan Stanley warns of power constraints in 2027–2028, and Reuters reported that some U.S. data centers are already planning their own gas generation because the grid cannot keep up.

Political and social constraints are no longer hypothetical. A June 2026 Reuters/Ipsos poll found only 33% of Americans favored the rapid pace of data-center construction, 57% opposed such a facility in their own community, and 77% worried AI would raise electricity prices; Reuters also reported UN researchers’ warning that data-center power and water use could roughly double by 2030. These pressures matter because a visible bubble collapse does not require unused capacity; it only requires assets to come online too slowly, too expensively, or into a much lower-price market than sponsors expected.

Competitive dynamics and historical analogies

The closest historical analogies are solar PV, LCD panels, and memory. In each case, the underlying technology was real and transformative; the problem was that industrial policy, scale effects, and price competition compressed returns. The IEA says China now holds more than 80% share across major solar manufacturing stages, after an enormous shift of capacity away from Japan, Europe, and the United States; the OECD adds that solar was the most subsidized industrial sector from 2005 to 2024 and that excess capacity pushed prices below break-even for several Chinese firms in 2024. Reuters’ reporting on LG Display’s exit from saturated LCD production captures a similar pattern of competition forcing legacy players into higher-margin niches.

AI is not identical to solar panels, but the structural rhyme is strong: one layer captures value temporarily through scarcity, then capability diffuses through software, open weights, distillation, and cheaper hardware. Chinese vendors such as DeepSeek can combine low pricing with domestic chip ecosystems; open-weight communities amplify diffusion; and governments can intensify the race through export controls, subsidies, and “sovereign AI” programs. The visible bubble risk is therefore not that AI demand disappears, but that commercial advantage diffuses faster than physical capital can earn back its cost.

Scenario comparison

The table below is illustrative rather than predictive. It is anchored to Goldman’s baseline build-out, IEA capex and power data, current token-price compression, and evidence of rising political frictions.

| Scenario | Investment levels | Price trajectory | Market concentration | Likely timeline |

|---|---|---|---|---|

| Best-case reset | High but disciplined; build-out slows into utility-like cadence after 2027 | Frontier prices ease; commodity prices fall but stabilize | Moderate concentration in premium tier, broad competition below | Stress in 2026–2027, orderly normalization by 2028–2030 |

| Base-case squeeze | Very high capex through 2027, then selective cancellations and asset write-downs | Commodity token prices keep falling; premium models retain some pricing power | Barbell market: a few frontier clouds, many low-cost and local options | Visible equity/project-finance correction around 2027–2028 |

| Worst-case crack | Overbuild followed by financing retreat and stranded projects | Price war continues even as capital tightens; ROI collapses for many providers | Upstream chip and power suppliers concentrate; mid-layer model vendors wash out | Sharp capital-markets repricing in 2026–2028, long digestion into 2030+ |

Business outcomes, mitigation, and source priorities

The most likely durable outcome is three-tier segmentation. Premium frontier models remain expensive and concentrated; commodity cloud models become brutally competitive; and local/on-device models absorb a growing share of everyday enterprise and consumer workloads. That implies hybrid architectures: route routine tasks to local or cheap models, reserve premium cloud inference for high-value reasoning, and build the enduring moat in workflow, data rights, orchestration, and distribution rather than in generic model access alone.

For policymakers, the mitigation agenda is clear: accelerate transmission and permitting where justified; require transparency on data-center power and water use; avoid indiscriminate subsidy races; and prioritize interoperability so enterprises can switch between frontier, commodity, and local models without lock-in. For corporations, the corresponding strategy is to shorten asset lives in planning models, assume faster price decay, diversify across model classes, and design around hybrid inference rather than a single frontier-cloud dependency.

Assumptions and unspecified items

- Assumption: “Bubble collapse” means a visible repricing of AI equities, project finance, and infrastructure expectations, not the disappearance of AI usage. This is an analytical inference from current capex, price, and infrastructure data.

- Assumption: Scenario ranges are illustrative and not formal forecasts. They extrapolate from current capex, power bottlenecks, and price trends through 2032.

- Unspecified: Exact ROI thresholds for individual hyperscalers, sovereign-AI programs, or private data-center vehicles are not publicly disclosed in consistent detail.

- Unspecified: The pace of regulatory change in export controls, energy permitting, and local moratoria remains highly political and can shift abruptly.

Prioritized source set

| Source type | Why it matters most | Example |

|---|---|---|

| Official energy and infrastructure reports | Best primary evidence on power constraints, grid timelines, and system bottlenecks | IEA, Tracking Trillions; IEA, Key Questions on Energy and AI |

| Official vendor documentation | Best evidence for local/on-device trends and chip efficiency claims | Microsoft Foundry Local; Apple Foundation Models; Google Gemma docs; NVIDIA Blackwell docs |

| Reuters reporting | Best for current capex, financing, pricing wars, and political backlash | DeepSeek pricing, OpenAI burn, Reuters/Ipsos poll, U.S. grid strain |

| arXiv economics papers | Best current quantitative work on token-price trends and cost behavior | Tiered Super-Moore’s Law; Price Reversal Phenomenon |

| Historical policy analogies | Best evidence for subsidy-driven overcapacity and commoditization | IEA Solar PV; OECD solar subsidies brief |

In short, the most visible AI bubble-collapse scenario is not technological failure. It is success without sufficient capture: AI keeps spreading, prices keep falling, and the physical capital stack proves too expensive, too slow, and too exposed to political friction for much of the sector to earn its promised returns.